Like a peanut butter and jelly sandwich without the peanut butter.

The biggest problem I see in fundraising decks is too much text. The next biggest problem is a fundraising deck without a fundraising slide. Using another food analogy, it’s like a menu from a steakhouse not listing any steaks – um, this is a steakhouse, isn’t it?

I see three reasons for the fundraising slide omission. The first is that some people think it is somehow impolite or inappropriate to bring up fundraising in a, gasp, fundraising presentation. Instead, they focus on the gee-whiz of their great product and won’t speak about fundraising in polite company.

The second is that some CEOs think that it’s up to the investor to make an initial move on fundraising terms. That is often true, but that doesn’t mean that fundraising should be ignored in the presentation.

And the third is that the presenter just doesn’t know what to put in a fundraising slide or what to say.

Tackling the first reason first – it’s not inappropriate to talk fundraising. An investor audience that takes the time to listen to your investment pitch wants to hear your thoughts about the investment you are selling. Investors tend to evaluate companies pretty quickly. If an investor has all the information needed to make an initial assessment, they will. They may not remember a lot of your pitch, but they will remember that they either want to learn more or they want to pass. And an investor that passes does so either because they’ve heard something they don’t like or because they haven’t heard enough to form an opinion – and that itself can cause a pass. So if you don’t discuss fundraising and the audience can’t reach a conclusion, it’s often a pass.

For the second reason, it may be true and appropriate for the CEO to want the investor to make the first move. But the “move” usually comes down to the valuation number in a priced round or a valuation cap in an unpriced round. All the other significant elements of a fundraising should be discussed. These other elements don’t constitute making a first move, but do give the investor additional information to help them decide on the company’s attractiveness.

Finally, the presenter that doesn’t know what to say about fundraising risks alienating the audience two times over – the first because they don’t have needed information, and the second because the presenter comes across as naive because they haven’t provided the information, especially if after they are directly asked.

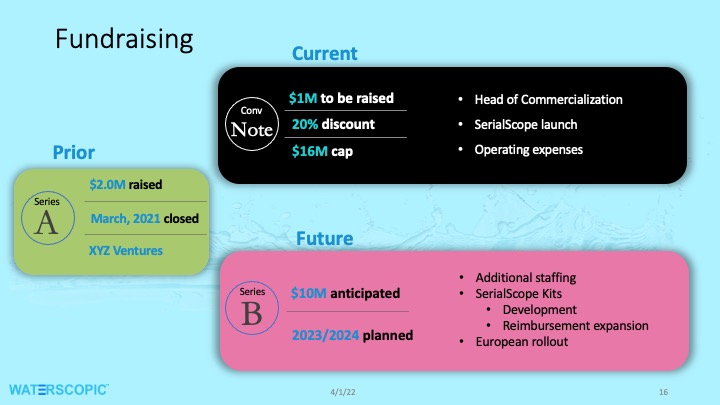

An initial investor presentation should always include a fundraising slide which should include:

- The timing of prior rounds and the amounts raised. It’s optional to include the names of key investors, but beneficial if those investors confer some credibility. It’s also optional to show the valuation of those prior rounds. The steeper the increase in valuation between those rounds, the more useful it may be to show those valuations.

- For the present round:

- The amount you intend to raise.

- Any money already raised in the round.

- If there are commitments or money-in-hand from prior investors .

- The timing and any terms that are firm about the round should be shown, such as the structure of the round and the discount offered if not a priced round. If the deal is set, documents have been drawn and money has already been received on those terms, this should be shown so investors know that other investors have already done diligence and set terms. If the company does not have a clear idea of the structure or terms, the slide should show that the deal terms are “to be negotiated,” but remember that this can lead to investors losing some interest.

- A basic description of the use of funds being currently raised should either be on the slide or in the following slide.

- If one or more future rounds are anticipated, an outline of the timing and amount of those rounds.

There a few items that should not be shown, such as if company intends to issue common stock and not preferred. Investors dislike common, so if a company is set on selling common, it may be wiser to save that for a follow-up discussion. An investor who gets enthusiastic enough to follow up may be willing to accept some unappealing terms that they would have found unacceptable earlier in the process.

Another issue is if the company is dead-set on a valuation that, at least at first glance, seems out of range for the perceived risk and opportunity. That is a situation where it may be better to reserve any valuation discussion for a follow-up.

In my experience, VCs are often less insistent on hearing a valuation number. If interested, they will determine what they believe to be a reasonable valuation. Angel investors are more likely to expect to be presented a valuation.

A hard and fast rule is – don’t skip the fundraising slide. Less clear is exactly how to handle some elements of the deal, and that is up to the discretion of the entrepreneur.

0 Comments